India Vegetable Oil Imports H1 2026: Bill Jumps 19% as Crude's Share Hits 97%

India bought more cooking oil this half-year and paid a great deal more for it. From November 2025 to May 2026, the country imported 9.37 million tonnes of vegetable oil, edible and non-edible together, up 12% from 8.34 million tonnes a year earlier. The import bill rose faster, to roughly ₹1.05 lakh crore, a jump of about 19%.

That gap between volume and value is the whole story. Prices did part of it. The rest came from the rupee, which averaged 95.53 to the dollar against 85.25 a year earlier, a 12% slide that makes every imported tonne dearer in local terms.

The duty wedge

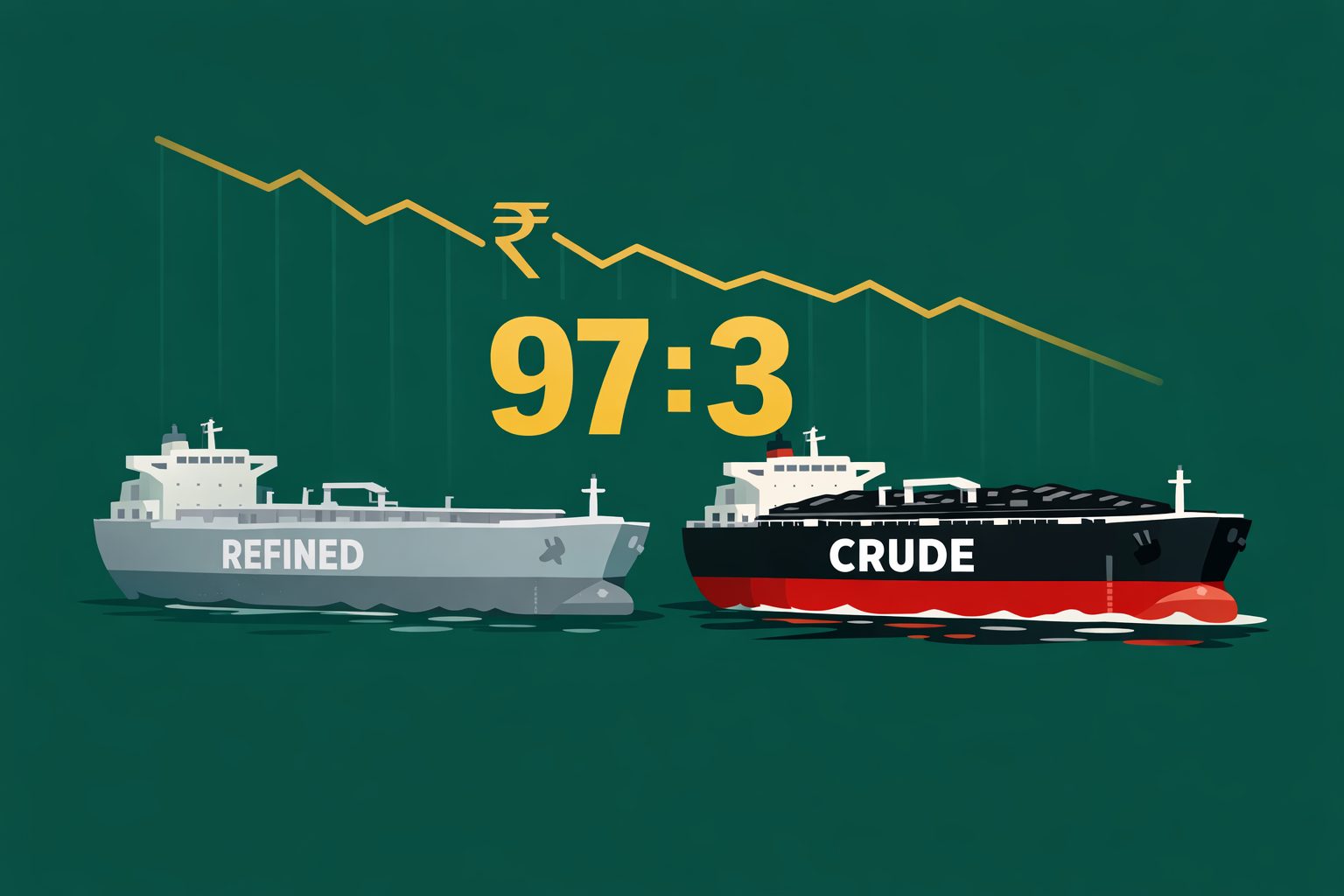

One number captures how the trade has changed shape. Imports of RBD palmolein, the refined, ready-to-use palm oil India once pulled in by the shipload, fell 94% to just 0.05 million tonnes, down from 0.95 million a year ago. Refined oil as a whole shrank to 3% of the edible basket from 16%. Crude now accounts for 97% of what India ships in, up from 84%.

This did not happen by accident. India taxes refined oil far more heavily than crude. The basic customs duty on refined grades sits at 32.5%, with an effective rate near 35.75%, while crude grades carry a 10% basic duty after the cut notified in May 2025. The spread between the two widened past 19 percentage points. For a refiner at home, that gap is a moat: importing crude and processing it locally beats buying finished oil from abroad, and the trade flow has bent to match.

Palm regains share

Within edible oils, palm clawed back ground it had lost. Palm took 49% of the basket over the seven months, against 41% a year earlier. Soft oils, mainly soybean and sunflower, slipped to 51% from 59%. The swing tracks price. When soybean and sunflower oil ran expensive through late 2025 and early 2026, buyers leaned back toward cheaper palm. In January alone, palm imports rose sharply while soybean oil fell to a 19-month low.

The supplier map

The supplier map reflects the shift:

- Argentina — 20.64 lakh tonnes (soybean-oil heavyweight, single largest origin)

- Malaysia — 17.60 lakh tonnes (palm)

- Indonesia — 17.18 lakh tonnes (palm)

- Russia — 9.60 lakh tonnes (sunflower)

- Brazil — 5.75 lakh tonnes

- Ukraine — 2.99 lakh tonnes

- Nepal — 2.80 lakh tonnes

Across the basket: palm 49%, soybean 31%, sunflower 20%.

The price ladder

Prices explain why the bill hurt. Average CIF costs in May were up sharply on the year: crude palm near $1,265 a tonne, crude soybean oil around $1,352, crude sunflower oil about $1,432, and RBD palmolein near $1,233. Each ran 19% to 23% higher than a year before. Pay that in a weaker rupee and the math turns ugly fast.

There was one cushion for buyers. Stocks rebuilt. Total holdings at ports and in the pipeline reached 2.21 million tonnes by early June, against 1.35 million a year earlier, helped by stronger pipeline movement. That gives importers room to wait out price spikes rather than chase every cargo.

What the half-year actually says

India is importing more oil, in cruder form, from a more concentrated set of suppliers, and paying a premium driven as much by the currency as by the commodity. The duty structure is doing its job of pulling refining back onshore, which helps domestic processors and the jobs around them. It does little for the household at the till, where the rupee and the world price still set the terms.

The next few months turn on three things: where palm trades as Indonesia diverts more oil into biodiesel, whether the rupee steadies, and how India's own winter oilseed crop comes in. Any one of them can move the bill again.

The convening point

GLOBOIL India 2026 is where India's import desk meets the people who set these numbers. The 29th edition runs 29 September to 1 October at The Westin Mumbai Powai Lake, bringing 2,000-plus refiners, traders and policymakers from 60 countries to argue out where the duty, the rupee and the basket head next.