The Three Mandates Re-Read: Biofuel Calendar Reshaped

Three weeks ago, the consensus framing in global vegetable oil markets was clear: three biofuel mandates would land in a single 30-day window, collectively pulling 4.3 million tonnes of vegetable oil out of food markets into fuel. Malaysia B15 from 1 June. Indonesia B50 from 1 July. US EPA Set 2 already active for 2026. The framework supported the structural bull case. Dorab Mistry's MYR 5,200 call rested on it.

The framework has fractured. As of 25 May, only one of those three mandates is proceeding as originally planned. The other two have shifted in ways that materially recalibrate the demand-side narrative. The incremental biofuel pull for H2 2026 is now closer to 1.3 million tonnes than 4.3 million tonnes. This is one of the most significant analytical recalibrations in vegetable oil markets so far this year, and the consensus framing has not yet fully caught up.

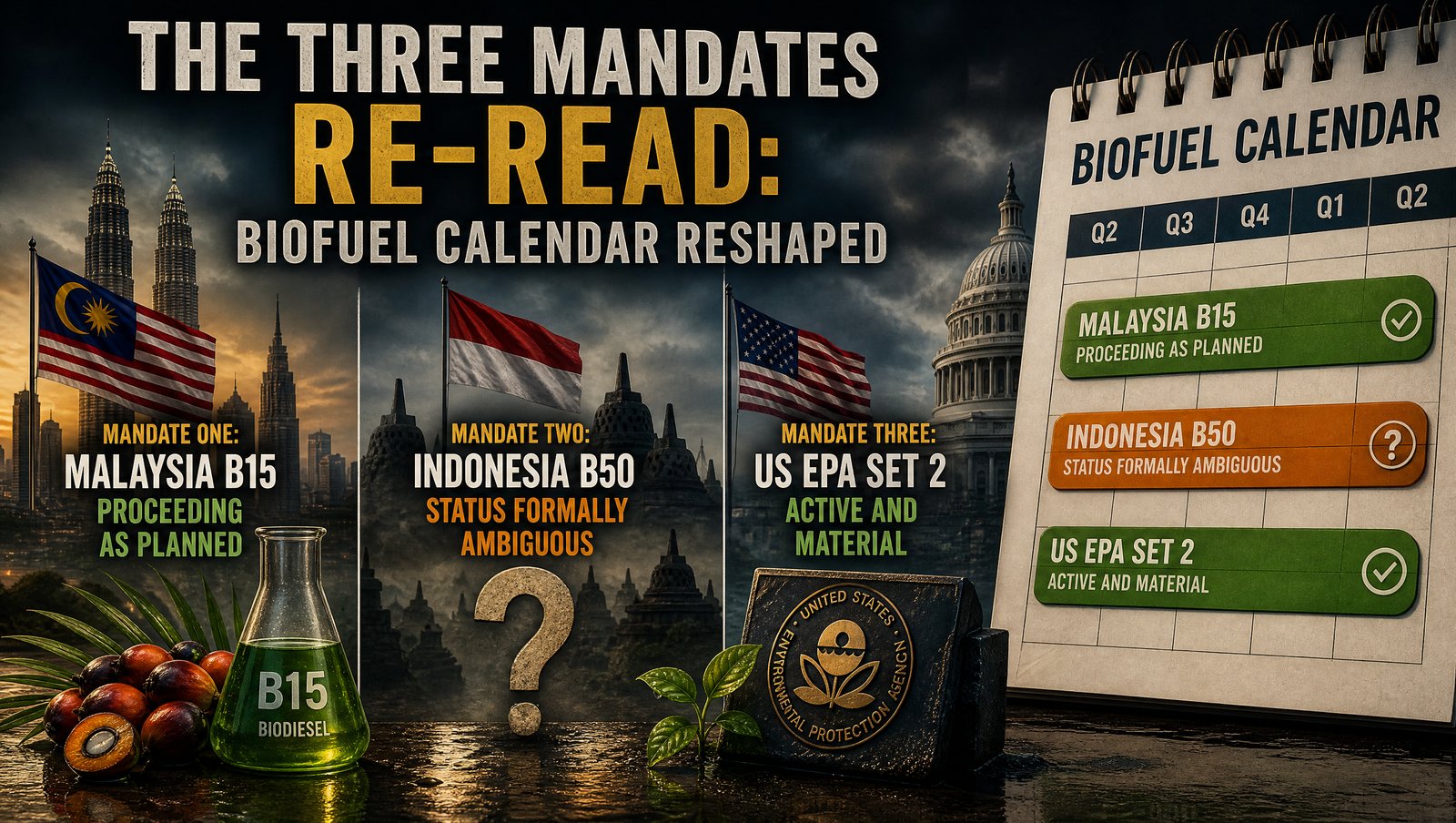

Mandate one: Malaysia B15 — proceeding as planned

Malaysia's B15 biodiesel mandate activates 1 June 2026, raising the mandatory blend from B10 to B15 with phased rollout through B12 to full B15 within the calendar year. The Malaysian Palm Oil Council estimates 300,000 tonnes of incremental annual domestic palm oil absorption, with the bulk of the impact materialising in H2 2026. MPOB's April data confirmed Malaysian biodiesel exports surged 193% month-on-month — evidence of active pre-positioning for the mandate activation.

Malaysian refiners and biodiesel producers are integrated and prepared. There are no implementation risks worth weighting. The B20 conversation is now active at the policy level, suggesting upside optionality through 2027.

Net contribution to H2 2026 incremental demand: approximately 200,000–300,000 tonnes.

Mandate two: Indonesia B50 — status formally ambiguous

This is the single most consequential change in the framework. On 14 January 2026, the Indonesian government — under presidential directive from Prabowo — formally maintained the B40 biodiesel mandate through the end of 2026, with B50 deferred to potential 2027 implementation. The decision was driven by three factors: BPDPKS subsidy fund constraints, ongoing fuel road trials for trains, heavy equipment, and industrial machinery, and uncertainty around the crude oil-CPO price spread that underpins biodiesel economics.

Between January and early May, however, the market read the policy environment as setting up B50 activation for 1 July 2026, supported by elevated crude oil prices making B50 economics more favourable. This was the framing used by Mistry on 6 May.

The 20 May Prabowo announcement on single-gate export reform has now reset the policy direction conclusively — Indonesia is prioritising structural fiscal reform over near-term mandate expansion. The most reasonable current read: B40 continues through 2026, B50 is deferred to 2027 subject to subsidy fund recapitalisation through the higher export levies (10% to 12.5% effective 1 March 2026), and the single-gate export reform consumes the policy bandwidth that might otherwise have advanced B50.

To compensate for the lost subsidy revenue base, Indonesia raised the CPO export levy from 10% to 12.5% effective 1 March 2026. This is a price impact on Indonesian exports but does not directly add demand.

Net contribution to H2 2026 incremental demand: approximately zero from B50. B40 continues at established absorption levels of roughly 15.65 million kilolitres annually.

Mandate three: US EPA Set 2 — active and material

The US Environmental Protection Agency finalised its Renewable Fuel Standard Set 2 rule on 27 March 2026, requiring biomass-based diesel blending of 5.61 billion gallons in 2026 (up 67% YoY) and 5.86 billion gallons in 2027 (up 75%). The rule has driven CBOT soybean oil futures to multi-year highs and supports approximately 1 million tonnes of incremental soybean oil pull into US biofuel feedstock relative to 2025 baseline.

This mandate is real, active, and contributing to the bullish vegetable oil narrative. CBOT soybean oil at multi-year highs cascades through global soybean oil pricing and supports palm oil through substitution effects.

Net contribution to H2 2026 incremental demand: approximately 1 million tonnes of soybean oil equivalent.

The revised arithmetic

Stacking the three mandates under the revised framework:

- Malaysia B15: 200,000–300,000 tonnes of palm oil incremental

- Indonesia B50: zero (deferred, effective B40 continues)

- US EPA RFS Set 2: approximately 1 million tonnes of soybean oil incremental

- Total: approximately 1.2–1.3 million tonnes of vegetable oil incremental demand in H2 2026

This compares to the original framework's approximately 4.3 million tonnes. The recalibration is a roughly 70% reduction in biofuel-driven incremental demand for H2 2026 relative to the consensus framing three weeks ago.

What this means for the bull case

The bull case for palm oil and broader vegetable oil pricing in H2 2026 has not collapsed — it has narrowed. The structural drivers remain in place:

- Indian demand is firm at H1 levels of 7.94 million tonnes annualised — directly supportive

- Indonesian export uncertainty under the single-gate reform creates near-term supply friction

- El Niño risk for late 2026 and H1 2027 remains an active variable

- US EPA Set 2 continues to support CBOT soybean oil pricing through year-end

- Malaysian B15 adds modest but real domestic absorption

What has changed is the magnitude of the supply-tightening case. Without B50, the global vegetable oil deficit projection for the 2025-26 marketing year narrows materially — from roughly 3 million tonnes to roughly 1 million tonnes. The food-versus-fuel competition framing weakens. The price ceiling adjusts downward.

For Bursa Malaysia CPO, the revised framework suggests a price corridor for Q3 2026 of approximately MYR 4,400–4,800 rather than the MYR 4,800–5,200 corridor that the original framework implied. For CBOT soybean oil, the upside remains supported by domestic US biofuel demand but the global premium narrows. For Indian retail edible oil prices, the inflation pass-through moderates relative to the bullish scenario.

Three scenarios for H2 2026

Scenario A — Revised base case (probability: 55%). Indonesia single-gate framework rolls out gradually through 2026 with manageable market disruption. B40 continues, B50 stays deferred. Malaysia B15 proceeds. US EPA Set 2 supports soy. Indian H1 demand strength extends into H2 at a measured pace. Bursa CPO range MYR 4,400–4,800. CBOT soy oil holds at multi-year highs but does not extend further.

Scenario B — Bull case partial recovery (probability: 25%). Indonesia announces B50 acceleration in Q3 2026 in response to fiscal pressure or subsidy fund recapitalisation. Single-gate implementation creates 30–60 day supply friction. El Niño conditions develop earlier than expected affecting Q4 production. Bursa CPO targets MYR 4,800–5,200 by November. Indian retail inflation runs 6–10%.

Scenario C — Bear case extension (probability: 20%). Indonesia single-gate implementation proceeds smoothly. Malaysian production strength extends through Q3. Indian demand consolidates at H1 levels without acceleration. US-Iran tensions ease, Brent drops below $90, biofuel economics weaken. Bursa CPO ranges MYR 4,000–4,400. Vegetable oil prices broadly soften through year-end.

What to watch through Q3

- Indonesian Government Regulation on single-gate export — timing and design

- Indonesian commentary on B50 timeline — any signal of acceleration or further deferral

- Malaysia B15 actual rollout — domestic absorption pace

- US EPA RIN credit pricing — leading indicator of biodiesel mandate fiscal sustainability

- SEA India monthly import data — H2 demand pattern confirmation

- CBOT soybean oil open interest — institutional positioning

- Brent crude weekly closes — the multiplier variable

The convening point

GLOBOIL India 2026 at The Westin Mumbai Powai Lake from 29 September to 1 October — exactly four months after Malaysia's B15 activates, nine months after Indonesia's B50 deferral, and at the precise moment when the revised biofuel demand framework crystallises in actual H2 demand data. The conference theme — At the Inflection Point: Energy, Sustainability & India's Demand Future — was set six months ago. The market has now caught up to the question implicit in the theme.

Dorab Mistry's annual outlook, Thomas Mielke's Oil World forecast, panel discussions with CPOPC, MPOC, GAPKI, SEA of India, CME Group, USSEC, and Fastmarkets will frame the revised pricing logic for H2 2026 and into 2027. For procurement, trading, and risk teams reviewing forward positions, this is the most important room of the year.

Two of three biofuel mandates have shifted. The bull case has narrowed, not broken. The price corridor recalibrates. The desks that recalibrate first will trade the next 60 days correctly.

Editorial analysis by the GLOBOIL Intelligence Desk based on Indonesian Government policy releases, MPOB data, US EPA Set 2 rulemaking and USDA balance-sheet projections through 25 May 2026. Not investment advice.