Milei's Slow Unwind: How Buenos Aires Is Repricing the World's Soybean Oil

Argentina is the largest exporter of soybean oil and soybean meal on the planet, and it is in the middle of taking apart the tax system that has shaped those exports for years. The pace is deliberate, the direction is one-way, and the effect on global soft-oil prices is only starting to land.

The plan

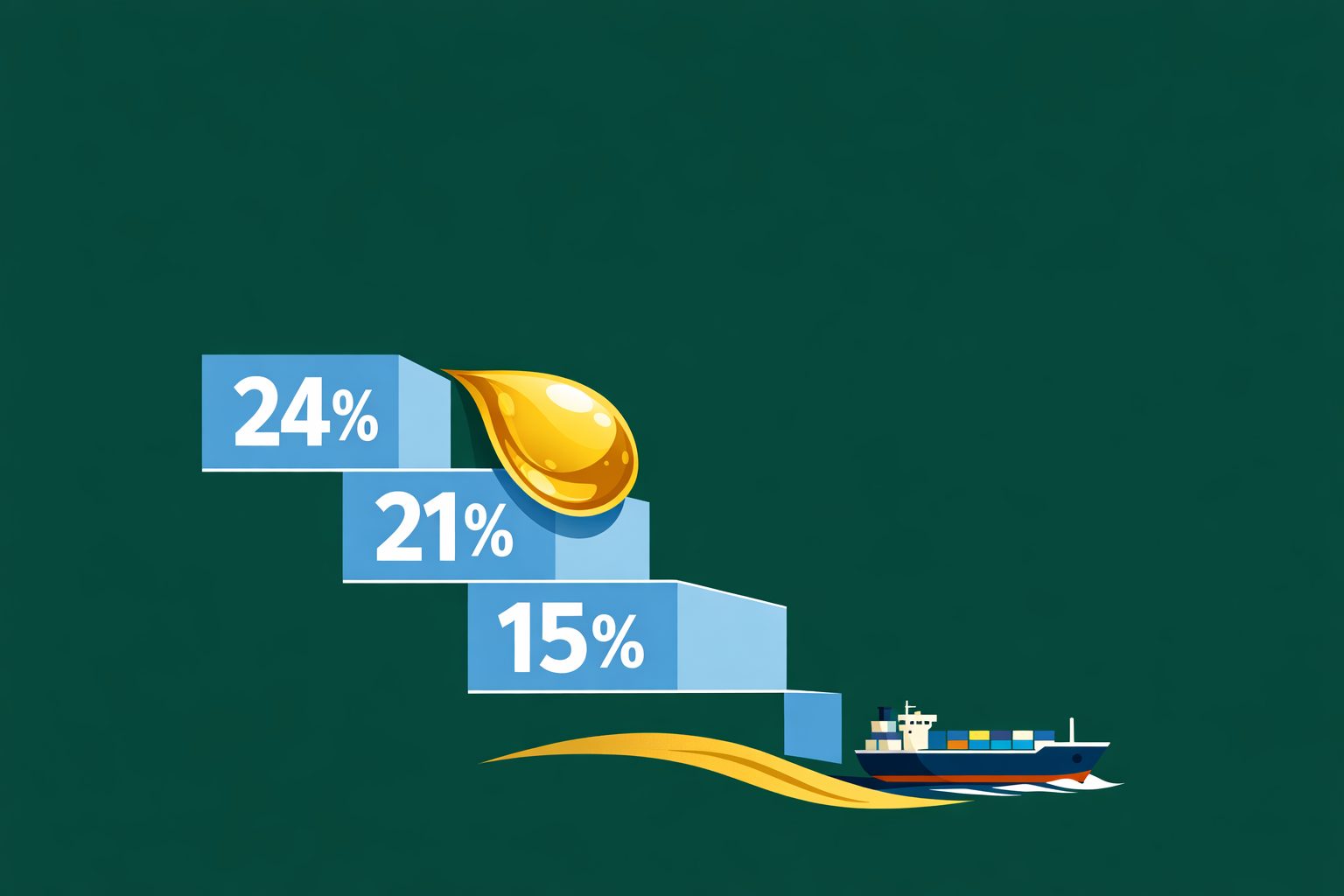

Under the plan, the export tax on soybeans falls from 24% to 21% by early 2027 and to 15% by the end of 2028. Taxes on the processed products, soybean oil and meal, come down in step, heading toward roughly 14% by late 2028. The cuts arrive in small monthly increments, a quarter of a point at a time in 2027, then half-point steps in 2028. It is the agriculture plank of President Javier Milei's broader push to scrap export taxes altogether.

Why it matters

Export taxes on processed oil and meal act as a thumb on the scale for the whole crush chain. Lower them, and Argentine soybean oil lands cheaper at destination. For a buyer in Asia weighing soybean oil against palm or sunflower, a few dollars a tonne decides which cargo books.

India in the path

India sits squarely in the path. In the most recent half-year, Argentina was India's single largest source of imported vegetable oil, ahead of the palm suppliers Malaysia and Indonesia. That makes Argentine tax policy an Indian price story as much as a South American one. As soft oils take a larger share of Indian kitchens, cheaper Argentine soyoil gives importers a deep, reliable pool to draw on.

The transition risk

The transition has not been smooth. A brief, earlier suspension of export taxes triggered a rush of selling that drew down stocks, and prices whipsawed as traders tried to read whether the cuts would stick or be clawed back. That episode is a warning: policy this consequential, moving in monthly steps, creates a year of small shocks rather than one clean reset.

Crush economics holding

Crush economics are holding up regardless. Brazil's biodiesel mandate keeps domestic demand for soybean oil firm, which supports crush margins across South America and keeps plants running hard. Regional crush is expected to hold around 42 million tonnes. Strong margins mean more oil and meal produced, which over time adds to exportable supply even as taxes fall — a double tailwind for buyers.

The bigger picture

For the soft-oil complex, the read is bearish on price and bullish on availability. More competitively priced South American soybean oil pressures sunflower and palm to stay cheap to compete. It also matters because the other soft oil, sunflower, has turned unreliable out of the Black Sea, and palm is being pulled into Indonesian fuel tanks. Soybean oil is becoming the steady leg of the stool.

The risks running the other way

Argentine policy can reverse on a bad fiscal quarter; export taxes are a dependable revenue source, and governments under pressure reach for them. Weather is the other wildcard, since a dry season on the Pampas can erase the supply gains a tax cut promises. Buyers should treat the cheaper-oil trend as real but not guaranteed.

For now, the direction is set. The world's biggest soybean-oil exporter is making its oil cheaper to ship, one month at a time, and the soft-oil market is slowly pricing it in.

The convening point

South America sets the floor for soft oil, and India sets the demand. GLOBOIL India 2026 is where those two ends of the trade meet. The 29th edition takes place 29 September to 1 October at The Westin Mumbai Powai Lake, gathering the crushers, shippers and buyers who move soybean oil from the Pampas to the Indian coast.